Untap · Money Owed · 13 May 2026

Money Owed · Class Actions

Five places where money has been set aside, or is being decided, for tens of millions of UK consumers

£7.5 billion set aside, letters starting 30 June 2026

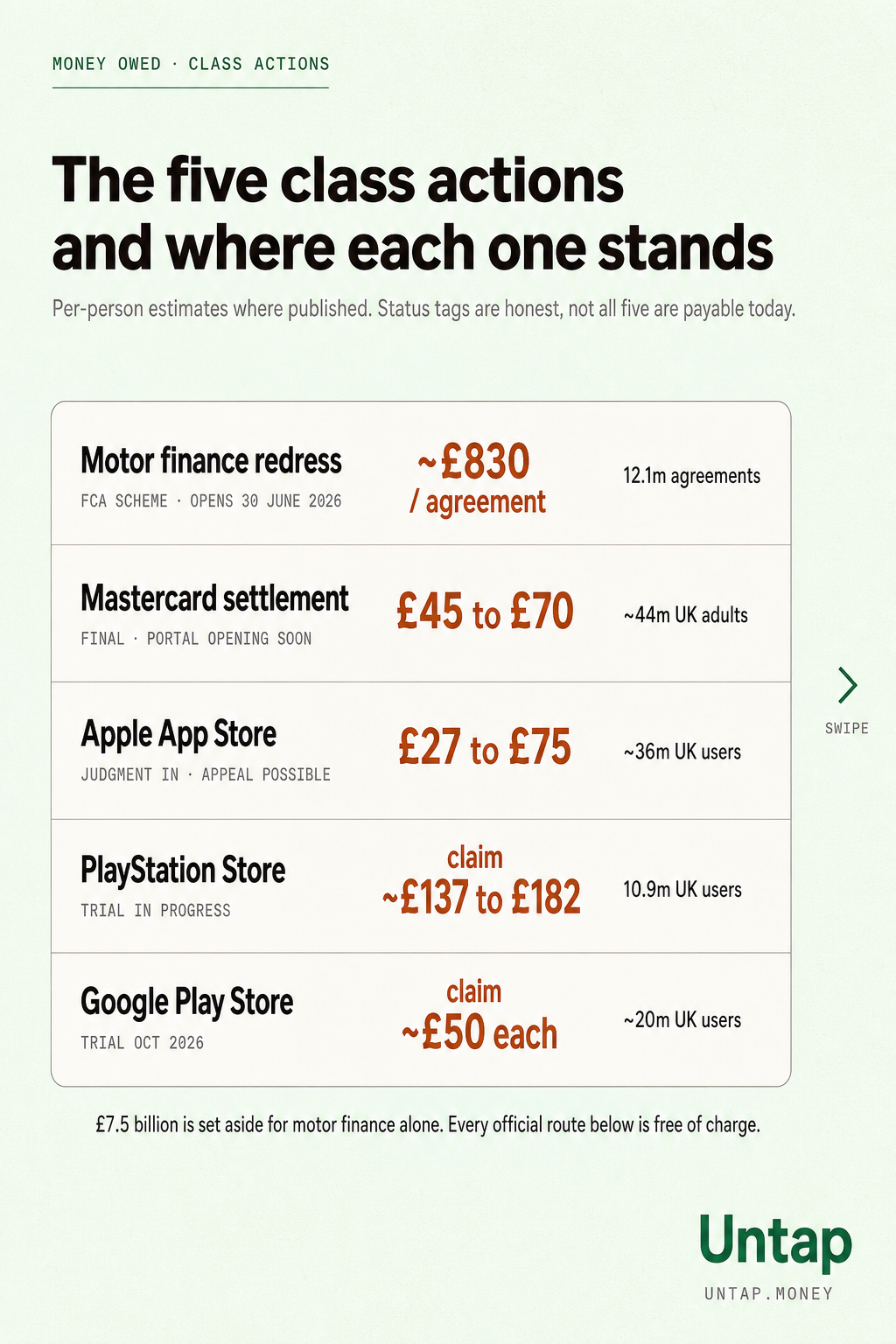

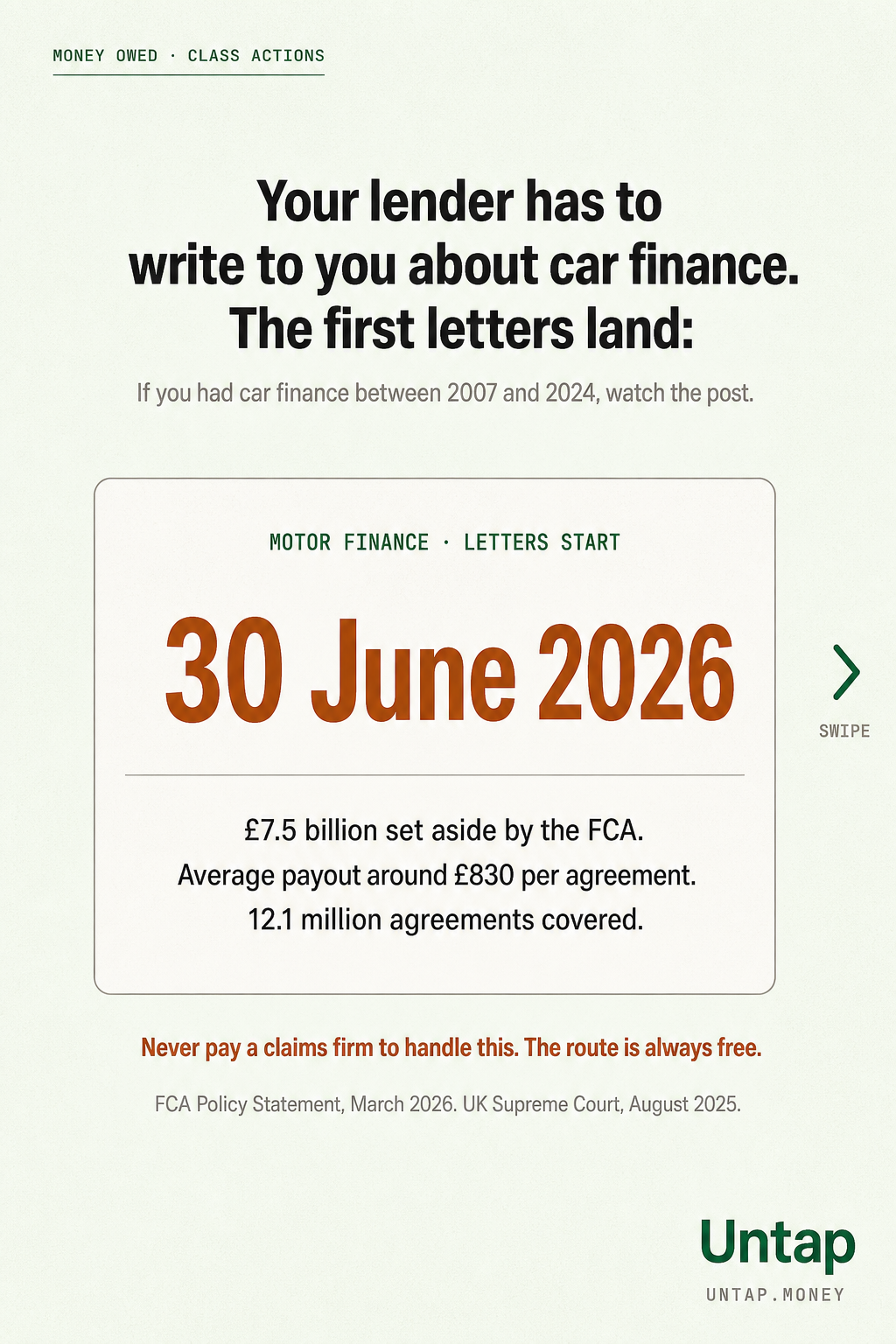

On 30 March 2026 the Financial Conduct Authority confirmed its biggest single consumer redress scheme in over a decade (Source: FCA Policy Statement PS26/3, Motor Finance Consumer Redress Scheme, 30 March 2026.). The scheme covers hire-purchase and PCP (personal contract purchase) motor finance agreements taken out between 6 April 2007 and 1 November 2024. The regulator estimates that 12.1 million agreements are eligible, with UK lenders ordered to pay back £7.5 billion in total.

The trigger was the UK Supreme Court ruling in August 2025 in the joined cases of Hopcraft, Johnson and Wrench (Source: Hopcraft and others v FirstRand Bank and Close Brothers [2025] UKSC 33, 1 August 2025.). The court rejected the broader argument that car dealers owed customers a fiduciary duty, but held that Mr Johnson’s relationship with his lender was “unfair” under the Consumer Credit Act, because the commission paid to the dealer was large and undisclosed. The FCA scheme follows from that finding.

The average payout is around £830 per agreement. A person with two or three car-finance agreements in the window could receive more than that in total. Some customers will receive less; some materially more, depending on the size of the commission and the agreement.

The scheme is lender-led, not portal-led. UK lenders must proactively contact customers from 30 June 2026 for agreements taken out between April 2014 and November 2024, and from 31 August 2026 for agreements between 2007 and 2014. You do not need to register on a website. You do not need to pay a claims-management firm to find out if you are owed money. The letter will come.

That makes scam letters and texts a near certainty between now and the end of the year. Any message asking you to pay to “unlock” your motor finance refund, or to share bank details to receive it, is a scam. The real letter will come from your lender, will not ask for upfront payment, and will be checkable against your finance agreement.

Mastercard is paying, Apple has won, PlayStation and Google are still in trial

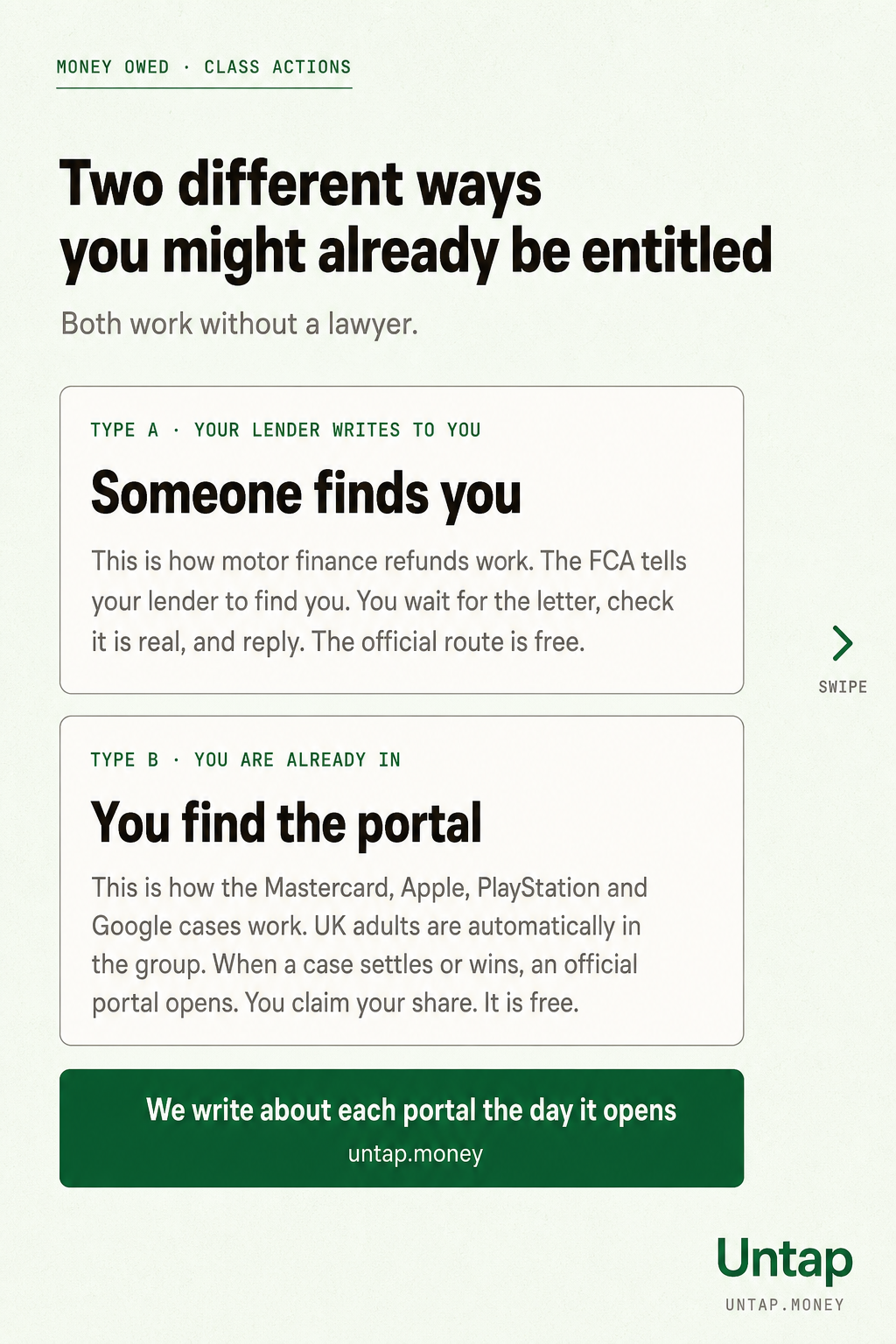

The four other cases on the list all sit at the Competition Appeal Tribunal, the UK court that handles competition-law claims. Each runs as an opt-out class action: UK adults in the eligible group are automatically in, without having to sign up, and only need to claim their share when an official portal opens after a settlement or judgment.

Mastercard. The longest-running of the four. The Competition Appeal Tribunal approved a £200 million settlement on 21 February 2025; the final order making the settlement binding came on 31 October 2025 (Source: Walter Hugh Merricks CBE v Mastercard, Competition Appeal Tribunal case 1266/7/7/16.). The eligible class is around 44 million UK adults aged 16+ who lived in the UK at any point between 22 May 1992 and 21 June 2008 and who bought goods or services from a UK business that accepted Mastercard. You did not need to own a Mastercard. The expected per-person payout is £45 to £70. The official site is mastercardconsumerclaim.co.uk; you can register interest there now, and the claims portal is expected to open later in 2026.

Apple App Store. The first ever opt-out class action damages award in UK history was handed down on 23 October 2025 (Source: Kent v Apple [2025] CAT 67.). Around 36 million UK iPhone and iPad users in the class period (1 October 2015 to 15 November 2024) were ruled to have been charged unfairly because of Apple’s 30% App Store commission. The damages range awarded was £1.18 billion to £2.24 billion (the tribunal gave a range, not a single figure). The tribunal refused Apple permission to appeal on 13 November 2025. Apple applied to the Court of Appeal in December 2025; on 23 March 2026 the Court of Appeal adjourned to a rolled-up hearing, so the appeal is live. The distribution portal will open after that route closes. The expected per-person payout is £27 to £75.

PlayStation Store. A claim brought by Alex Neill, the former chief executive of Which?, alleges that Sony charged excessive prices on the PlayStation Store between 19 August 2016 and 12 February 2026 (Source: Alex Neill Class Representative Ltd v Sony, Competition Appeal Tribunal case 1527/7/7/22.). The class is around 10.9 million UK PlayStation users. The trial began on 2 March 2026 and is listed for ten weeks. No money has been set aside yet, and there will be none until a judgment is handed down. The claimed per-person figure of £137 to £182 is the class representative’s estimate; the tribunal has not yet found in either direction.

Google Play Store. The companion case to Apple, brought by Liz Coll (Source: Coll v Alphabet and others, Competition Appeal Tribunal case 1408/7/7/21.). Around 20 million UK Google Play users and businesses for purchases between 1 October 2015 and 30 January 2026 are in the class (the class period was extended in April 2026; the opt-out deadline was 15 May 2026). Aggregate damages claimed are around £1 billion. The trial is scheduled for 5 October 2026; until judgment, no money has been set aside. A naive divide of the claim across the class works out at roughly £50 per user, but this is an Untap estimate, not a tribunal finding.

You are already in unless you actively opted out

For UK competition class actions at the Competition Appeal Tribunal (Mastercard, Apple, PlayStation, Google), you are automatically part of the group if you meet the eligibility description. You did not have to sign up to be entitled. What you do have to do, when a settlement or judgment is reached, is claim your share through the official distribution portal. If you do not claim by the deadline, your share is redistributed across the rest of the class or returned to other parties, depending on the court order.

The motor finance scheme is different. It is a regulatory scheme run by the FCA under section 404 of the Financial Services and Markets Act 2000, where the lender finds the customer rather than the other way round. You do not need to register anywhere.

In both kinds of case, you should never pay a claims-management firm a percentage of your payout to handle the registration. The official routes are free in every case, and the firms cannot do anything you cannot do yourself in five minutes when the portal opens.

The PACCAR effect

In July 2023 the Supreme Court ruled that the way most UK class-action funders are paid (a percentage of the damages) was not enforceable in opt-out cases. That froze the pipeline of new claims for about 18 months. In December 2025 the UK government confirmed it would legislate to reverse the effect. New cases are beginning to filter through, but the next wave is moving more slowly than it otherwise would have.

R (PACCAR Inc) v CAT [2023] UKSC 28

The scam-letter problem

Between now and the end of 2026, every claims-management firm in the UK will try to get between you and your motor-finance refund. The right answer in every case is the same. Use the official site only. Do not pay an upfront fee. Do not share bank details on a phone call you did not start. Your lender will write to you; the court portals will publish their own URLs.

FCA; Competition Appeal Tribunal; Money Saving Expert

Check the official site for each case, register where the portal is open, wait where it is not

- Motor finance: fca.org.uk/consumers/car-finance-complaints. Wait for your lender to write to you from 30 June 2026. Verify any letter against your finance agreement.

- Mastercard: mastercardconsumerclaim.co.uk. Register your interest now. The claims portal opens later in 2026.

- Apple App Store: appstoreclaims.co.uk. The distribution portal will open once Apple’s appeal route closes.

- PlayStation: playstationyouoweus.co.uk. Trial in progress; sign up for updates.

- Google Play: appstoreclaims.co.uk/google. Trial October 2026; sign up for updates.

Untap writes about each portal the day it opens. Sign up for the weekly digest at untap.money if you would rather not check five sites yourself.

Reproduce every figure in this piece

- FCA Policy Statement PS26/3 · Motor Finance Consumer Redress Scheme, 30 March 2026. £7.5 billion total redress, 12.1 million agreements, average £830 per agreement. Open

- Hopcraft and others v FirstRand Bank and Close Brothers [2025] UKSC 33 · UK Supreme Court, 1 August 2025. The ruling that triggered the FCA scheme. Read

- Walter Hugh Merricks CBE v Mastercard · Competition Appeal Tribunal case 1266/7/7/16. £200 million settlement, ~44 million UK adults, £45–£70 per person. Official site

- Kent v Apple [2025] CAT 67 · Judgment of 23 October 2025. UK’s first opt-out class action damages award. ~36 million users, £1.18–£2.24 billion range. Tribunal page

- Alex Neill Class Representative Ltd v Sony · Competition Appeal Tribunal case 1527/7/7/22. Trial commenced 2 March 2026, ~10.9 million UK PlayStation users. Official site

- Coll v Alphabet and others · Competition Appeal Tribunal case 1408/7/7/21. ~19.5 million UK Google Play users, trial October 2026. Official site

- R (PACCAR Inc) v CAT [2023] UKSC 28 · UK Supreme Court, 26 July 2023. The ruling that slowed the UK class-action pipeline; pending government reversal. Read

Money Owed · Class Actions is the third instalment of Untap’s Money Owed series. The £7.5 billion motor finance figure and the £200 million Mastercard figure are final and confirmed by the FCA and the Competition Appeal Tribunal respectively. The £1.2 to £2.2 billion Apple range is the tribunal’s awarded range. The PlayStation and Google per-person figures are the class representatives’ own estimates and are not tribunal findings. The carousel and this piece make these distinctions explicit throughout. Comments and corrections to contact@untap.money.

Published 13 May 2026.